Trade Idea: A Narrow Calendar in a High Volatility Market

Originally posted on June 9, 2020

This market has been crazy for a couple of months now and this means that traders need to adapt to the conditions. I believe good traders can trade in almost any environment. A big part of my options journey is to learn how to trade in as many different market environments as possible. Only then can I consistently make money no matter what the market does.

As one who has only been trading consistently for about 5 years now this is, by far, the longest stretch I’ve ever seen with high market volatility. As many of you know I primarily trade SPX and my trading plans were built around normal volatility ranges with the VIX in the range of about 10-25. This market hasn’t been in this range since the start of the virus crash which is now been about 3 months. When it started, I did some of my usual alternative trades: trades on non-correlated things like metals, even doing some directional plays like synthetic covered call like I discussed in my last blog post. But this market is now in very new territory for me. VIX has settled down in the mid to upper 20s which is pretty low for the last 3 months but is still historically high. So what’s an SPX trader like myself to do? I usually don’t start going negative Vega trades like Butterflies until VIX is in the low 20s and forget calendars with their high positive Vega, right? Well…maybe not.

At least for now, a relatively low VIX is in the 20s. But that’s still pretty high. Calendars are tempting because volatility is relatively low compared to the last couple of months but it’s still high enough that calendars give you lots of room. But nothing is free in this market. The reason the market gives me a ton of room on calendars is because while a 25 VIX may feel low right now, it’s still quite high and so the risk of a big move is still around. Add in the fact that volatility is mean reverting and we could have the risk of dropping volatility while we’re very long Vega. That wide tent could contract and put the trade into trouble quicker. As I’ve stated in a previous blog post, when I set up my usual calendar in a low volatility market, I like to put my longs 2 weeks away from my shorts. This give me a nice mix of price and Vega exposure. The further out in time, the more expensive the calendar and the more Vega you get. This is because the longs will have more extrinsic value than the shorts so they will cost more and that extrinsic value will decay faster as the distance between them increases so you get more of a time difference and positive volatility exposure. So how could a calendar be adapted to fit the market today? Here’s a modified setup that has been working well for more recently. I’ve named it a “narrow calendar” and it has the following differences from my standard calendar:

- It is shorter in duration

- The longs are very close to the shorts

To show some examples I need to set some guidelines. I could simply compare two calendars: one with 14 days between the shorts and the longs and one with three days. You will see a huge difference in the Greeks but I’m not this is a fair comparison because the risk is so much smaller. As you can see below:

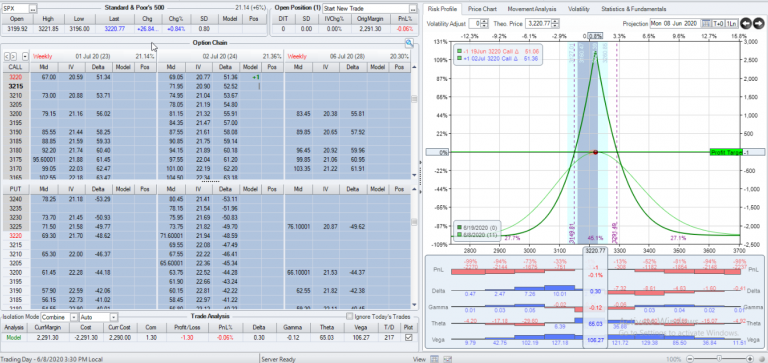

An 11-day calendar with the longs 2 weeks out

This is an 11-day calendar with the longs 2 weeks from the shorts. The cost is $2291.30, I get very flat delta since it’s at the money and my Theta is 65 and my Vega is 106. Compare that with a one lot where I put the longs 3 days away and I get this:

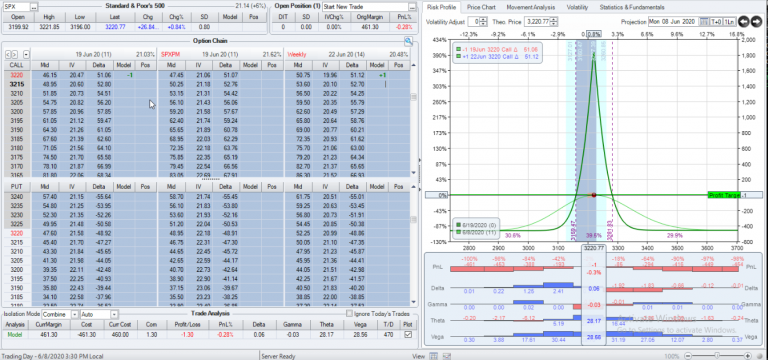

An 11-day Calendar with the longs 3 days out

So you can see here, I have drastically less Theta and Vega but the cost is about 20% lower since the long is so much cheaper. This can be a benefit if you want to keep you risk down, but it’s not really a fair comparison with respect to the Greeks since they are proportional to size. So I think a fairer comparison is to make the narrow calendar a 5-lot to get similar risk size:

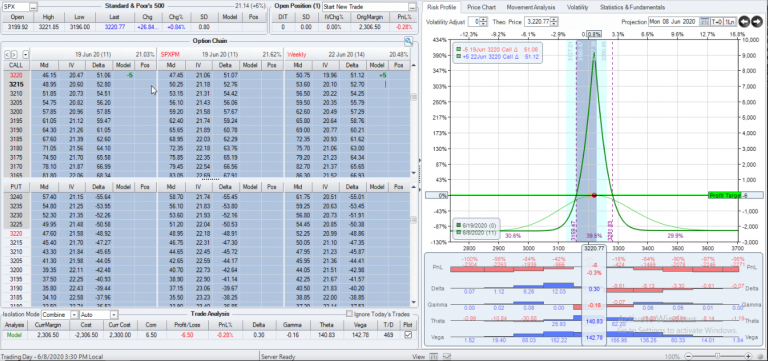

An 11-day Calendar with longs 3-days out (5-lot)

Now with a 5-lot the cost is $2306.50 which isn’t exactly the same but close enough that I think it’s a fairer comparison. The Vega is higher, but if you look at the ratio of Theta to Vega: it’s much better, almost 1:1. Yes, I have a bit more overall Vega risk but the Theta benefit more than makes up for it so my risk/reward ratio is better. And because this is a 5-lot, I’m able to scale this down to lower my risk while the first example is a 1-lot which can’t be scaled down.

So why wouldn’t I always do this style of calendar? The reason there is the volatility level of the market. I usually do calendars when VIX is under 13.5. In that environment, I don’t mind taking on more Vega risk relative to Theta because VIX is low and will most likely pop. But with VIX in the 25-30 range, I like to lower that ratio to help cushion the blow of a volatility drop. Also, when VIX is very low, I expect the size of the tent will be much narrower which will make this structure less appealing than it is now. So I would prefer to get more room by going back to a two week time spread.

Another thing to consider: with most underlyings you may only have Friday expirations so the shortest time you would have is one week. This is why I like doing this in SPX (or if you want to scale it down even more, you can use SPY), because it has Monday and Wednesday expirations so it’s possible to get very short distances between the shorts and the long.

Of course, I cannot say if this trade is right for you or not. Everyone’s experience level is different. If you aren’t familiar with spreads or calendars, you may want to paper trade a few to get the idea. Also feel free to check out my Options Fundamentals series where I try to explain these concepts in more detail for beginners. But it’s a good lesson in the Greeks and hopefully can spark some thinking about how to adapt a trade to different market conditions. If you would like to see how these trades have worked out, check out my This Week @MidwayTrades series around the end of May into early June. You can see my put these on and how I manage them.

As usual, I’d love to hear any feedback or questions on this or about options trading in general. Feel free to reach out here on the site or you can email me at midway@midwaytrades.com.

This content is free to use and copy with attribution under a creative commons license.